The trinity of errors in applying confidence intervals: An exploration using Statsmodels

O'Reilly on Data

DECEMBER 9, 2019

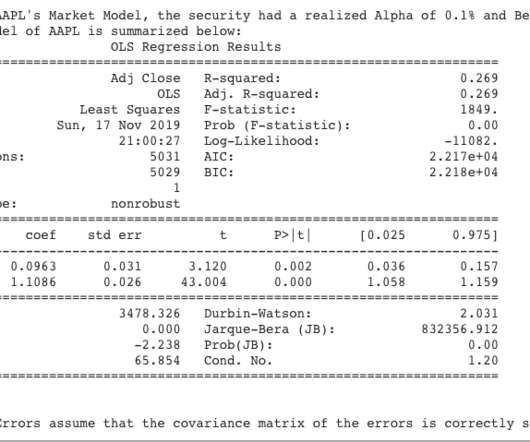

Recall from my previous blog post that all financial models are at the mercy of the Trinity of Errors , namely: errors in model specifications, errors in model parameter estimates, and errors resulting from the failure of a model to adapt to structural changes in its environment. For example, if a stock has a beta of 1.4

Let's personalize your content